Most young adults do not get a financial handbook when they start earning. One day, money starts coming in, and suddenly there are bills, subscriptions, savings goals, and countless spending decisions to make. It can feel exciting and overwhelming at the same time. The good news is that building a strong financial future is less about earning a huge salary and more about developing the right habits early.

Many people assume they will focus on personal finance later when they make more money. In reality, the habits formed during the first few years of earning often shape long-term financial success. Whether you are receiving your first paycheck, paying off student loans, or trying to build financial independence, a few smart decisions today can create lasting benefits for years to come.

Start With A Budget You Can Actually Follow

One of the most effective money management tips for young adults is learning where money goes every month. Many people underestimate how much they spend on small purchases, food delivery, subscriptions, and impulse buys.

A simple approach is the 50/30/20 rule:

- 50% for essential expenses such as housing, transportation, utilities, and groceries

- 30% for lifestyle spending, entertainment, hobbies, and travel

- 20% for savings, investments, and debt repayment

This framework helps create balance between enjoying life today and preparing for the future. Tracking expenses through budgeting apps or spreadsheets can reveal spending patterns that often go unnoticed.

Build Strong Saving Money Habits Early

Saving money becomes much easier when it happens automatically. Instead of waiting until the end of the month to save what is left over, reverse the process and pay yourself first.

Set up an automatic transfer to a savings account every payday. Even a small amount saved consistently can grow significantly over time. This approach removes the temptation to spend money before saving it.

Another useful habit is separating needs from wants. Before making a non-essential purchase, give yourself at least 48 hours to think about it. Many impulse purchases lose their appeal after a short waiting period.

Developing strong saving money habits early creates financial flexibility and reduces stress when unexpected expenses appear.

Create An Emergency Fund Before Chasing Investments

Many young adults become interested in investing before building a financial safety net. While investing is important, having emergency savings should come first.

An emergency fund acts as protection against job loss, medical bills, car repairs, or unexpected life events. Financial experts generally recommend saving three to six months of living expenses in a separate account that is easy to access.

Without emergency savings, people often rely on credit cards or loans when problems arise. That can quickly create debt that becomes difficult to manage.

Building an emergency fund may take time, but it provides peace of mind and protects your long-term financial goals.

Learn To Manage Debt The Smart Way

Debt management is a major part of financial planning for young adults. Not all debt is harmful, but high-interest debt can slow down financial progress.

Credit card balances are especially costly because interest charges accumulate quickly. If you currently carry debt, focus on paying it down using a structured approach.

Two popular methods include:

- Debt Avalanche: Pay off the debt with the highest interest rate first.

- Debt Snowball: Pay off the smallest balance first to create momentum and motivation.

Both approaches work. The best choice is the one you can stick with consistently.

At the same time, paying bills on time should become a non-negotiable habit. Late payments can lead to fees and negatively affect your credit profile.

Build Credit Before You Need It

Many young adults do not think about credit until they need a car loan, apartment lease, or mortgage. By then, building a strong credit history becomes more difficult.

Opening a credit card and using it responsibly can help establish a positive credit record. One important rule is to keep credit utilization below 30% of your available limit.

It is also essential to pay the full statement balance every month rather than only the minimum payment. This prevents costly interest charges while helping build a strong financial reputation.

Anyone interested in learning how to maintain good credit should focus on timely payments, low credit utilization, and responsible borrowing habits. These simple actions can significantly improve long-term borrowing opportunities.

Start Investing Earlier Than You Think

One of the biggest advantages young adults have is time. The earlier investing begins, the more powerful compound interest becomes.

When investment earnings generate additional earnings, growth accelerates over time. Even modest monthly contributions can produce meaningful results over several decades.

Many beginner investors assume they need thousands of dollars to start. In reality, consistent investing matters far more than starting with a large amount.

Low-cost index funds and diversified investment accounts often provide an accessible starting point for beginners. Setting up automatic monthly contributions removes emotion from the process and helps maintain consistency.

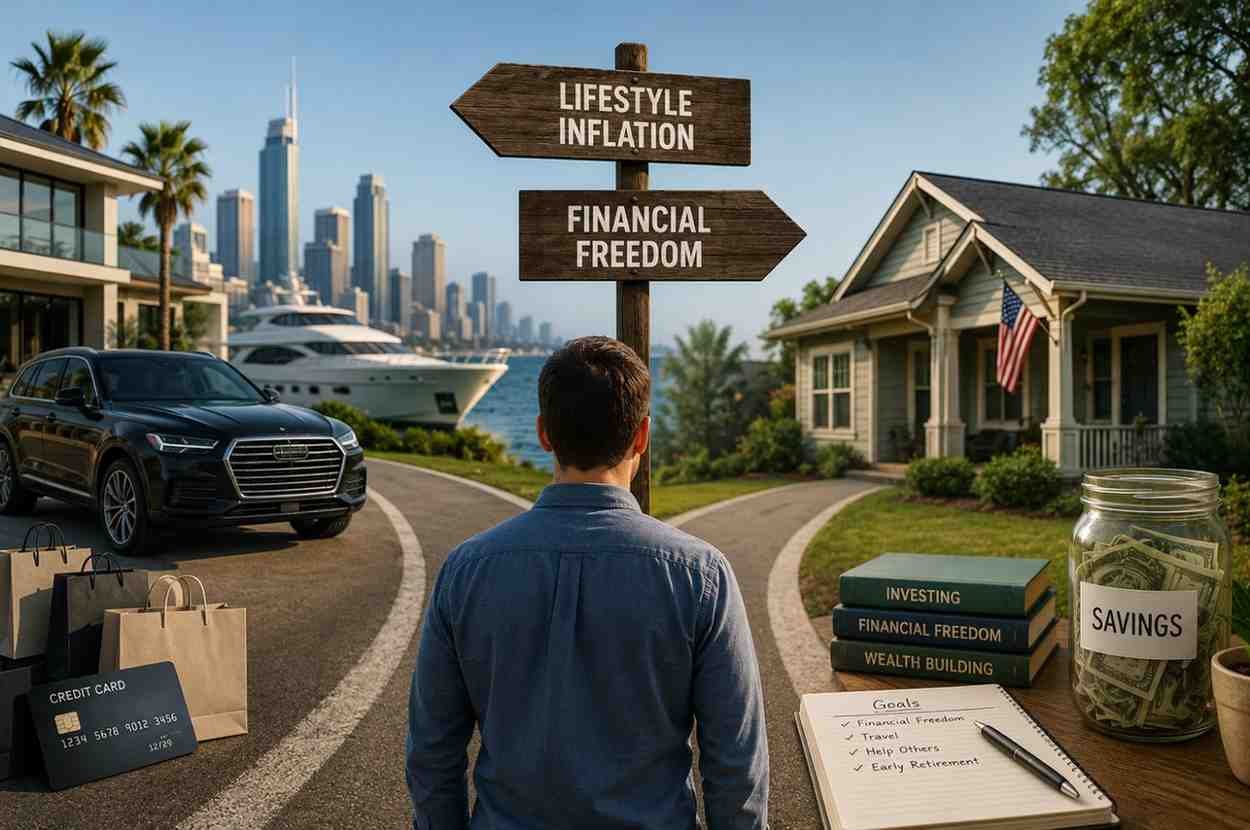

Avoid Lifestyle Inflation As Income Grows

Receiving a raise often creates the temptation to immediately increase spending. Bigger apartments, newer cars, and more frequent shopping can quietly absorb additional income.

This pattern is known as lifestyle inflation. While occasional upgrades are reasonable, allowing every pay increase to become new spending can limit wealth-building opportunities.

Instead, consider directing a portion of every raise toward:

- Retirement savings

- Investment accounts

- Emergency savings

- Debt repayment

This strategy allows your financial future to improve alongside your income.

A Simple Financial Roadmap For The First Few Months

Starting personal finance for young adults does not need to be complicated. A practical roadmap can make the process easier.

Month 1: Gain Expense Awareness

Track every transaction for 30 days. This creates a clear picture of spending habits and cash flow.

Month 2: Build Emergency Savings

Open a dedicated savings account and work toward your first emergency fund milestone.

Month 3: Establish Credit Responsibly

Open a credit account if needed and commit to paying every statement balance on time.

Month 4 And Beyond: Begin Investing

Start with small, automated contributions to a diversified investment account and increase contributions whenever possible.

Frequently Asked Questions: Smart Money Management Tips For Young Adults Starting Their Financial Journey

1. What Is The Best Budgeting Method For Young Adults?

The 50/30/20 budgeting method is often recommended because it balances essential expenses, lifestyle spending, and financial goals in a simple framework.

2. How Much Should Young Adults Keep In An Emergency Fund?

Most financial professionals suggest saving enough to cover three to six months of living expenses for unexpected situations.

3. When Should Young Adults Start Investing?

The best time to start investing is as early as possible. Beginning early allows compound growth to work for a longer period.

4. How Can Young Adults Improve Their Credit Score?

Pay bills on time, keep credit utilization low, avoid excessive borrowing, and regularly monitor credit activity for accuracy.

Final Thoughts

Building financial stability is rarely about making one perfect decision. It comes from a series of small actions repeated consistently over time. Budgeting, tracking expenses, saving regularly, managing debt, building credit, and investing early may seem simple individually, but together they create a powerful foundation for long-term success. The earlier these habits become part of everyday life, the easier it becomes to navigate financial challenges and take advantage of future opportunities.

Financial confidence grows one smart decision at a time. Start small, stay consistent, and allow time to work in your favor.